With the development of new energy vehicles, new energy battery technologies are constantly evolving. A growing number of R&D professionals are focusing on new energy battery materials in pursuit of groundbreaking innovations. As a key raw material in the battery sector, nickel sulfate has seen a new growth spurt in demand, which has brought about earth-shaking changes across the entire industrial chain.

New Demand Growth Driver for Nickel: Overview of Nickel Sulfate as a Key Raw Material in the Battery Sector

1.1 Properties of Nickel Sulfate

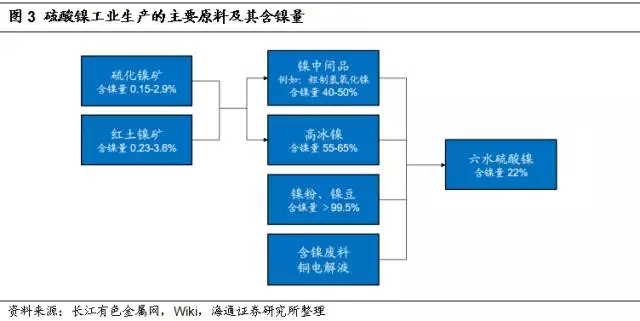

Nickel sulfate, with the chemical formula NiSO₄, exists in three forms: anhydrous, hexahydrate (NiSO₄·6H₂O) and heptahydrate (NiSO₄·7H₂O), with densities of 3.68, 2.07 and 1.948 g/cm³ respectively. Most commercially available nickel sulfate is in the form of hexahydrate, which has a molecular weight of 262.84. Both the output and price of nickel sulfate are referenced to the hexahydrate form. It has two crystal structures: α-form (tetragonal crystal, blue) and β-form (monoclinic crystal, green).

When the temperature is below 31.5℃, nickel sulfate solution crystallizes into heptahydrate. Nickel sulfate heptahydrate is a green, transparent crystal with a sweet and astringent taste and slight deliquescence.

Between 31.5℃ and 53.3℃, it crystallizes into α-form nickel sulfate hexahydrate (a blue, opaque crystal); it transforms into the β-form at 53.3℃, loses 5 molecules of water of crystallization to become monohydrate at 103℃, and loses all water of crystallization to form a yellowish-green anhydrous substance at 280℃. It decomposes into sulfur trioxide and nickel oxide at 840℃.

All three forms of nickel sulfate are readily soluble in water, and their aqueous solutions are weakly acidic (pH 4.5). The anhydrous form is insoluble in ethanol, ether and acetone; the hexahydrate is easily soluble in ethanol and ammonia water; the heptahydrate is soluble in alcohols. Nickel sulfate is toxic and possibly carcinogenic, with a maximum allowable concentration of 0.5 mg/m³ in air.

1.2 Preparation Methods of Nickel Sulfate

There are five methods for preparing nickel sulfate:

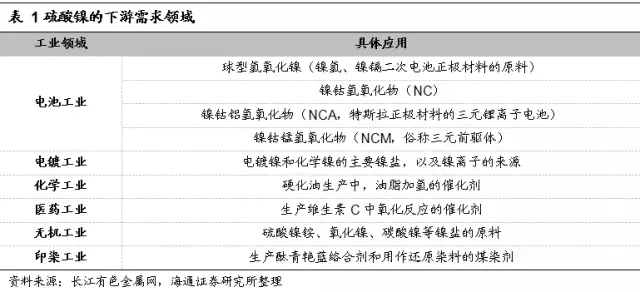

(1) Dissolve metallic nickel in sulfuric acid, crystallize to obtain crude nickel sulfate crystals, redissolve the crystals, remove impurities and concentrate to obtain battery-grade nickel sulfate crystals.

(2) Impurity metallic nickel in copper electrolysis is oxidized at the anode and dissolved into nickel sulfate; remove impurities and concentrate to obtain battery-grade nickel sulfate crystals.

(3) Process nickel ore into nickel intermediates such as matte nickel, nickel hydroxide, nickel oxide or nickel carbonate, then dissolve them in sulfuric acid, concentrate and crystallize to obtain nickel sulfate hexahydrate. Major domestic nickel sulfate producers such as Jinchuan Nickel Salt, Jien Nickel Industry and Guangxi Yinyi all adopt this method for nickel sulfate production.

(4) Prepare from nickel-containing solution generated during the production of metallic cobalt.

(5) Prepare from nickel-containing waste materials, with representative domestic enterprises including GEM Co., Ltd., Chizhou Xien and Brunp Recycling.

At present, countries and regions including Canada, South Korea, Japan and Taiwan all adopt the method of dissolving metallic nickel in sulfuric acid to produce nickel sulfate. This preparation method boasts advantages such as high raw material purity, low impurity content, stable supply, high-quality nickel sulfate output, and low pollution during production, while its disadvantage lies in relatively high manufacturing costs.

Nickel sulfate production in China mainly relies on intermediate-based preparation processes, which include: recovering impurity nickel contained in copper electrolysis; utilizing nickel-containing solutions generated during cobalt production; dissolving nickel intermediates such as nickel oxide, nickel hydroxide and nickel carbonate in sulfuric acid; and recycling nickel-containing waste materials. The primary advantages are diverse raw material sources and low production costs, whereas the main drawback is high pollution during the production process. With the continuous tightening of national environmental protection requirements for industrial production, domestic nickel sulfate enterprises are currently facing a trend of transitioning to using metallic nickel as the raw material.

2. Clear Direction Toward High-Nickel Ternary Materials: Demand Is Expected to Surge in the Future

2.1 Main Applications of Nickel Sulfate: Battery-Grade and Electroplating-Grade

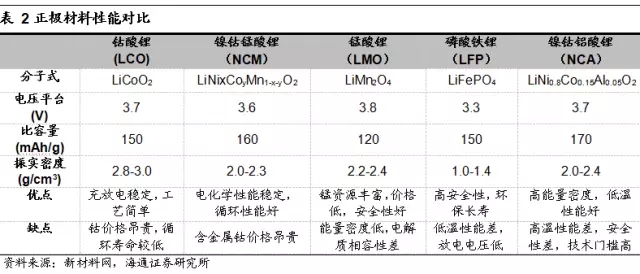

Nickel sulfate is classified into battery-grade nickel sulfate (Ni content ≥ 22%, Co content 0.4%) and electroplating-grade nickel sulfate (Ni content ≥ 21%, Co content ≤ 0.05%) based on the purity of nickel and cobalt, which are respectively applied in the battery and electroplating sectors. Electroplating-grade nickel sulfate is mainly used in the production of automotive wheel hubs, exterior components and other products.

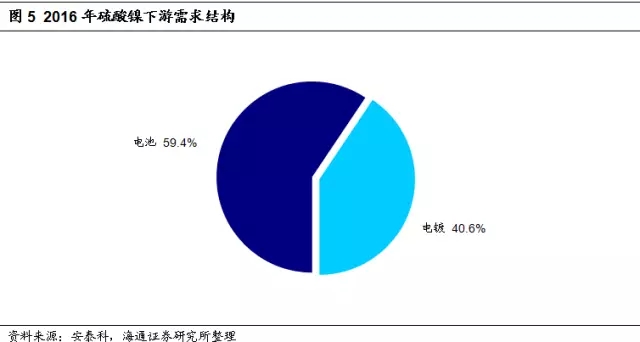

In the battery industry, nickel sulfate is mainly used in two categories of batteries: traditional nickel-cadmium batteries, nickel-metal hydride batteries, and the current mainstream ternary lithium batteries. Among them, nickel-cadmium batteries have been gradually phased out due to issues such as memory effect during charging and environmental hazards. The nickel element in spherical nickel hydroxide—the key raw material for the positive electrode of nickel-metal hydride batteries—and in lithium nickel cobalt manganese oxide (NCM) or lithium nickel cobalt aluminum oxide (NCA)—the precursor materials for ternary lithium-ion batteries—is all derived from nickel sulfate. The primary role of nickel in these materials is to enhance energy density, which determines the battery’s capacity.

2.2 New Energy Vehicles Drive Demand, with Cathode Materials Shifting Toward High-Nickel Ternary Systems

2.2.1 High Energy Density – A Top Priority for New Energy Vehicle Development

The core of new energy vehicles replacing fuel-powered vehicles lies in improving cost-performance ratio, defined as the ratio of driving range to cost. This means boosting driving range in terms of performance while reducing material costs and optimizing supporting system quality. To achieve this, it is essential to substantially increase the vehicle’s battery capacity—i.e., energy density—without adding to the system weight. National policy guidelines clearly stipulate that by 2020, the overall vehicle energy density should reach 260 Wh/kg, nearly doubling the then-current level, while costs should be reduced to ¥1 per Wh.

The implementation of the updated Dual-Credit Policy has amplified major automakers’ demand for high-energy-density batteries. Currently, the biggest bottleneck for high-energy-density batteries is the cathode material. The mainstream cathode materials on the market have a specific capacity of approximately 130–140 mAh/g, far lower than the 330–340 mAh/g of graphite anodes. The nickel content determines the number of active molecules in the cathode material and, consequently, its specific capacity. The shift of cathode materials from lithium iron phosphate to ternary materials, and from low-nickel ternary systems to high-nickel ternary systems and NCA, is an irreversible trend.

Data from the China Association of Automobile Manufacturers (CAAM) and the Electric Vehicle Resource Network shows that in the first half of the year, China’s new energy vehicle production reached 204,000 units, a year-on-year increase of 13.3%, while sales hit 195,000 units. Though slightly short of the full-year sales target of 800,000 units, the figure still represented substantial year-on-year growth.

With the phasing-out of subsidies for commercial vehicles, the lifting of restrictions on ternary cathodes, and the implementation of a series of subsidy policies focused on energy density and driving range, data from GGII (Guangzhou High-tech Industry Institute) indicates that the market share of ternary cathodes in power batteries surged from 22% in 2016 to an expected over 50% in 2017.

Different ternary materials vary in their demand for nickel sulfate. Calculations based on their molecular formulas show that per ton of cathode material, NCM333, NCM523, NCM622, NCM811 and NCA require 0.9, 1.36, 1.63, 2.16 and 2.03 tons of nickel sulfate respectively. It is evident that for ternary cathodes using nickel sulfate as a raw material, the nickel sulfate demand per ton of high-nickel ternary material is 2.4 times that of low-nickel NCM333.

At present, NCM333 and NCM523 remain the dominant ternary materials in the power battery sector. High-nickel material supply is severely insufficient, while competition intensifies as low-end production capacity is released. The supply of high-end materials is in acute shortage: in the previous year, the output of high-end ternary cathode materials such as NCA and NCM811/622 accounted for a mere 1% of the total ternary cathode material production. The demand for high-nickel materials is poised for robust growth in the future.

Cobalt prices have surged by over 100% compared with the levels at the start of the year, which has significantly increased the cost of ternary materials and squeezed manufacturers’ profit margins. Replacing cobalt with nickel can not only cut costs, but also further enhance energy density. Currently, due to constraints such as technical barriers, the nickel-cobalt ratio is still dominated by NCM333 and NCM523. According to data from GGII, the market share of NCM622 and NCA stood at around 5% in 2016, and this proportion is expected to rise substantially in the future.

The 18650 battery used in the Model S is a ternary battery model NCR18650B produced by Panasonic, with its cathode material being high-nickel NCA (LiNi₀.₈Co₀.₁₅Al₀.₀₅O₂). It has a capacity of approximately 3.3 Ah, a voltage of 3.6 V, and an energy density as high as 243 Wh/kg. The latest Model 3 is equipped with 21700 batteries, which still adopt NCA as the cathode material, with the energy density further increased to around 300 Wh/kg.

The NCA trend led by Tesla has a huge impact on the demand for nickel sulfate. First, we calculate the nickel sulfate demand for a single Tesla Model S: based on the number of battery cells, the capacity of individual cells, and the energy density of the cathode material, we can estimate that the Model S P85D requires 120.8 kg of NCA cathode material. Since 1 kg of NCA needs 2.03 kg of nickel sulfate as the raw material, a single Model S consumes 245.2 kg of nickel sulfate, equivalent to 2.88 kg per kWh. Based on this calculation, a Model 3 with a 75 kWh battery requires 216.4 kg of nickel sulfate. With the expected output of Tesla Model 3 hitting 1 million units in 2020, this alone will drive a global demand for 216,000 tons of nickel sulfate, accounting for nearly half of the current global downstream demand for nickel sulfate. Moreover, Tesla’s demonstration effect may prompt more automakers to adopt NCA cathode materials, and the global demand for nickel sulfate is expected to see an explosive growth in the coming years.

2.3 Total Demand Forecast: A 35.2% CAGR for Nickel Sulfate

The total demand for nickel sulfate is forecasted based on three categories: mainstream ternary cathode materials (including consumer lithium batteries and power lithium batteries), spherical nickel—the raw material for traditional nickel-metal hydride batteries, and the electroplating industry.

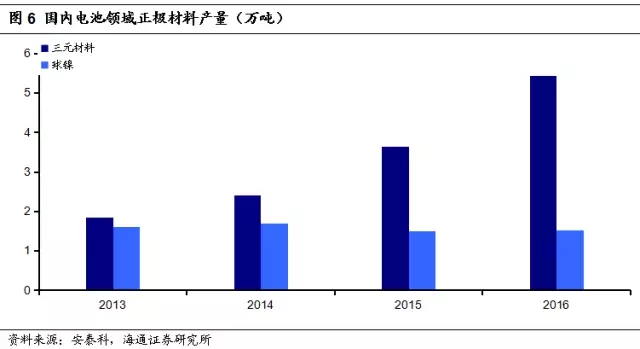

Data from the Electric Vehicle Resource Network shows that the national output of cathode materials reached 161,600 tons in 2016, a year-on-year increase of 43% compared with 2015; among this total, the output of ternary materials stood at 54,300 tons, representing a year-on-year growth of 49%.

According to data from GGII, China’s cathode material production is still dominated by NCM systems. In 2016, NCM333 accounted for 20%, NCM523 for 75%, and NCM622 plus NCA for 5%—with NCA making up less than 1% of the total. Based on the nickel sulfate consumption per ton of different ternary materials, the corresponding total demand for battery-grade nickel sulfate reached 69,900 tons.

The output of spherical nickel was 15,000 tons, almost flat compared with 2015. With a nickel content of 60%, this output translates to a consumption of 41,000 tons of battery-grade nickel sulfate.

Demand for nickel sulfate in the traditional electroplating industry remained stable, registering 76,000 tons in 2016 according to data from Antaike Information. In sum, the total domestic demand for nickel sulfate hit 187,000 tons in 2016.

Demand for traditional battery-grade nickel sulfate is expected to remain unchanged in 2017. The Yangtze Nonferrous Metals Network forecasts a 5% year-on-year growth rate for the electroplating industry each year. Driven by new energy vehicles, the demand for battery-grade nickel sulfate is poised to surge. Antaike expects the annual power battery shipment volume to reach 36 GWh in 2017, with ternary materials projected to account for around 50%—equivalent to 18 GWh, nearly three times the volume in 2016.

The annual output of ternary materials is estimated to hit 100,000 tons in 2017. Combined with the shifting proportion of ternary material types (driven by the trend toward high-nickel formulations), the total demand for nickel sulfate in 2017 can be calculated, with a compound annual growth rate (CAGR) of 35.2%.

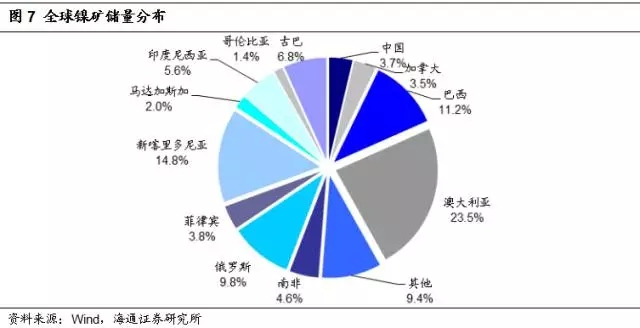

In nature, nickel exists primarily in two forms: oxide ores (laterite ores) and sulfide ores. Nickel ores in China are dominated by copper-nickel sulfide ores, among which the Jinchuan Nickel Mine in Gansu Province ranks as the world’s fourth-largest nickel sulfide ore deposit, accounting for 62.7% of the country’s total nickel reserves. Conversely, China is relatively deficient in laterite nickel ore resources and thus highly dependent on imports. In 2015, China’s nickel ore imports reached 35.1672 million tons, with external dependence exceeding 60%.

At present, the majority of nickel sulfate production in China adopts processes that do not use metallic nickel as the primary raw material. This approach offers advantages such as low production costs and diverse raw material sources, but it has drawbacks including significant environmental impact and relatively high requirements for enterprises’ technical capabilities. With the state’s increasing emphasis on environmental protection, China’s nickel sulfate production is trending toward a transition to using metallic nickel as the raw material. Nevertheless, nickel intermediates remain the primary feedstock for nickel sulfate production in China.

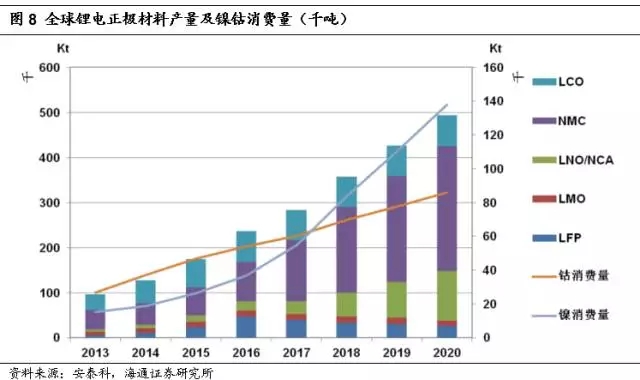

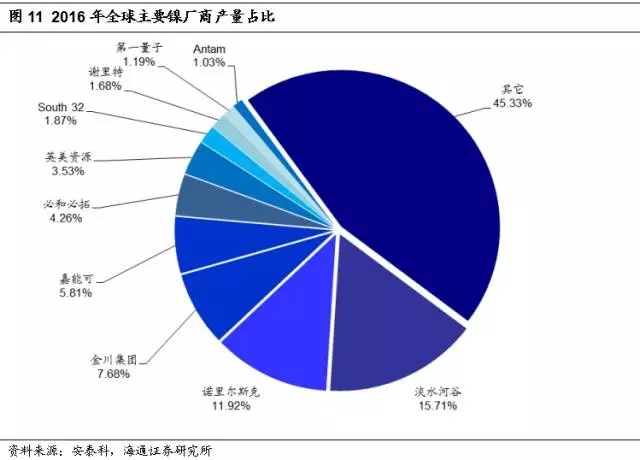

According to statistics from the International Nickel Study Group (INSG), the global output of primary nickel reached 1.98 million tons in 2016, with consumption standing at 2.0332 million tons. Currently, the 380,000 tons of global nickel sulfate production in 2016 accounted for less than 5% of total nickel consumption, a share far lower than that of the stainless steel sector. However, in terms of growth rate and consumption increment, it is unmatched by other downstream nickel application sectors.

In 2016, stainless steel accounted for 67.3% of global nickel consumption, while the battery sector made up 3.1%. Antaike forecasts that by 2020, the proportion of nickel used in the global stainless steel industry will drop to 64.2%, whereas the share consumed by the battery sector will rise to 7%. By 2025, nickel demand from the global battery industry is expected to hit 300,000 tons, accounting for 10% of total consumption, compared with 61% for the stainless steel sector.

According to Antaike Information, there was a clear inflection point in the growth rate of nickel consumption in the battery sector between 2016 and 2017, making the nickel market highly sensitive to demand for nickel sulfate. In addition, nickel ore supply from the Philippines and Indonesia remained uncertain in 2017, resulting in high elasticity in primary nickel supply. Given the current demand for battery-grade nickel sulfate, there is no immediate risk of raw material shortage.

However, the scenario is quite different for domestic nickel sulfate enterprises.

Nickel intermediates are mainly produced from laterite nickel ores through hydroxide precipitation technology, and laterite nickel ores are mostly dependent on imports. In recent years, the slump in nickel prices has forced many foreign small and medium-sized nickel mines to suspend operations. China’s nickel ore import volume has been declining year by year since 2013, leaving domestic nickel sulfate enterprises grappling with raw material shortages.

Currently, only Jinchuan Group has self-produced sulfide ores, and GEM Co., Ltd. operates nickel recycling production lines; thus, both have little demand for imports.

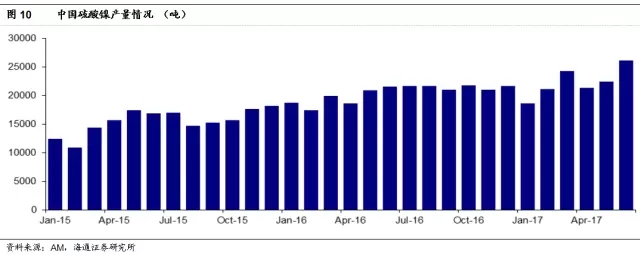

Data from the Asian Metal Network shows that China’s nickel sulfate output reached approximately 187,000 tons in 2015 and climbed to 247,000 tons in 2016. Before 2013, the country’s nickel sulfate output had remained basically stable at around 140,000 tons. As the output of new energy vehicles in China began to surge in 2014, nickel sulfate output increased accordingly, with the demand for ternary materials playing a remarkably significant driving role.

Currently, the domestic production capacity of nickel sulfate stands at approximately 343,000 tons. Driven by the booming development of power batteries and new energy vehicles, Jinchuan Nickel Salt, GEM Co., Ltd. and Guangxi Yinyi have subsequently planned an additional production capacity expansion of 90,000 tons for nickel sulfate.

According to Antaike’s estimation, China’s nickel sulfate output will rise to 300,000 tons in 2017; overseas output will reach around 200,000 tons, with production carried out by Sumitomo Group, Umicore, Norilsk Nickel and several other enterprises. Based on the subsequent production capacity expansion, we project that the global nickel sulfate output will further climb to approximately 600,000 tons in 2018.

Data from the Asian Metal Network shows that China’s nickel sulfate output reached approximately 187,000 tons in 2015 and climbed to 247,000 tons in 2016. Before 2013, the country’s nickel sulfate output had remained basically stable at around 140,000 tons. As the output of new energy vehicles in China began to surge in 2014, nickel sulfate output increased accordingly, with the demand for ternary materials playing a remarkably significant driving role.

Currently, the domestic production capacity of nickel sulfate stands at approximately 343,000 tons. Driven by the booming development of power batteries and new energy vehicles, Jinchuan Nickel Salt, GEM Co., Ltd. and Guangxi Yinyi have subsequently planned an additional production capacity expansion of 90,000 tons for nickel sulfate.

According to Antaike’s estimation, China’s nickel sulfate output will rise to 300,000 tons in 2017; overseas output will reach around 200,000 tons, with production carried out by Sumitomo Group, Umicore, Norilsk Nickel and several other enterprises. Based on the subsequent production capacity expansion, we project that the global nickel sulfate output will further climb to approximately 600,000 tons in 2018.

3.3 Nickel Sulfate Premium Stimulates Conversion from Electrolytic Nickel Production

At present, the price of electrolytic nickel is around ¥87,000 per ton, while the price of nickel sulfate is ¥25,000 per ton, representing a nickel-based premium of approximately ¥27,000 per ton of nickel sulfate. This substantial premium has spurred electrolytic nickel producers to shift their production to nickel sulfate. According to Antaike Information, international nickel giants such as BHP Billiton and Norilsk Nickel have begun to turn their attention to nickel sulfate. Optimistic about the prospects of nickel sulfate, these two major players plan to redirect their raw materials and production capacity toward nickel sulfate in the future. BHP Billiton also intends to produce nickel sulfate in Australia, and after signing a cooperation agreement with BASF, Norilsk Nickel plans to expand its nickel sulfate output going forward. Given that electrolytic nickel is also one of the raw materials for nickel sulfate production, and that most overseas nickel sulfate manufacturers adopt this technical route, a potential shortage in electrolytic nickel supply may emerge in the future.

Among domestic enterprises, Jinchuan Group has an electrolytic nickel output of around 120,000 tons this year, making it the manufacturer best positioned for production conversion. However, future progress will depend on the pace of decision-making by its management. In contrast, small and medium-sized private enterprises, with their relatively smaller production scales, can flexibly adjust their output between electrolytic nickel and nickel sulfate based on market prices, and thus can switch production to nickel sulfate at a much faster rate.

The combined nickel output of Norilsk Nickel, BHP Billiton and Jinchuan Group accounts for 23.85% of the global total. The shift in their electrolytic nickel production capacity will exert a substantial impact on the global nickel market.

Besides the relative shortage of raw materials, environmental protection issues are also a major factor affecting China’s future nickel sulfate supply. As early as 2015, the Ministry of Industry and Information Technology (MIIT) included nickel sulfate in the Catalogue of Hazardous Chemicals. Therefore, extremely stringent environmental protection requirements are imposed on nickel sulfate throughout its production, transportation, storage and other processes. The environmental impact assessment (EIA) for new production capacity requires a relatively long cycle, which will greatly restrict the expansion of new nickel sulfate production capacity.

The intensity of environmental inspections in 2017, as well as the central government’s stance on this matter, far exceeded expectations. The nickel sulfate production capacity covered by the fourth round of central environmental inspections and the "2+26" Special Action Plan for Air Pollution Prevention and Control in the Beijing-Tianjin-Hebei Region accounted for as much as 43.73%. Some production facilities that fail to meet environmental standards will face suspension of operations. Moreover, in the previous three rounds of central inspections, some enterprises have already been ordered to halt production due to failure to comply with environmental protection regulations.

In addition to bottlenecks in capacity expansion, the nickel sulfate industry also faces relatively high hidden barriers to entry. Generally speaking, newly-built production capacity must meet the requirements for supporting waste gas and wastewater treatment systems, and undergo a long-cycle environmental impact assessment, which may take about two years. In contrast, the expansion cycle for existing producers based on their original capacity is generally only around 10 months. Therefore, the current capacity expansion in the industry is mainly driven by existing manufacturers.

3.5 The Supply-Demand Balance Gradually Shifts Toward Shortage

From the perspective of supply-demand balance, our earlier calculations indicate that domestic demand maintains a high growth rate of 35.2%. At present, the market still sees a slight oversupply, which is attributable to the market expectations for high-nickel ternary materials and the release of previous excess capacity. However, it is more important to note that this situation is gradually reversing. In the coming years, with the mass production of Tesla Model 3 and the continuous breakthroughs in domestic high-nickel ternary technology barriers, the Model 3 alone will generate an additional demand of 216,000 tons by 2020. Coupled with the current domestic NCA penetration rate of less than 1%, based on the existing supply situation and the pressure on the supply side from environmental protection policies, we anticipate that nickel sulfate may face a persistent shortage in the next few years.

4. Prices Are at Historically Low Levels, and a Scenario of Simultaneous Growth in Volume and Price Cannot Be Ruled Out

The price of nickel sulfate mainly depends on the prices of raw materials including nickel concentrate, sulfuric acid and nitric acid, as well as processing costs. Among the production costs of nickel sulfate, the cost of nickel concentrate accounts for the major proportion. The average market price of sulfuric acid in 2017 was only ¥270 per ton; additionally, the average market price of nitric acid in 2017 was approximately ¥1,500 per ton. The raw material costs of sulfuric acid and nitric acid together account for only a small fraction of the total production cost.

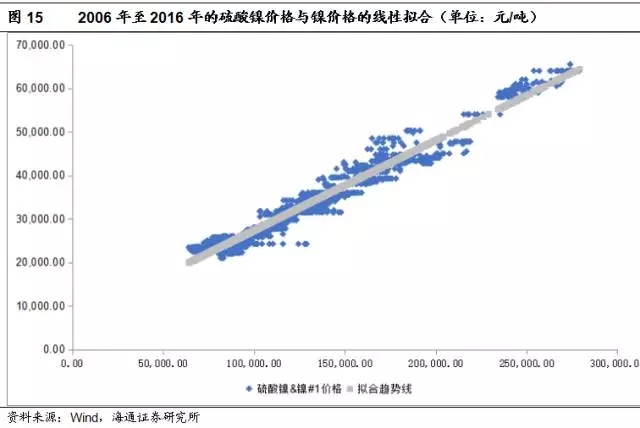

The price of nickel sulfate is highly correlated with that of nickel, which can be estimated using the following formula:

Domestic price (including tax) = [LME 3-month nickel price × 22.2% + processing fee] × (1 + 17%) × exchange rate

From the linear fitting chart of nickel sulfate price versus nickel price, we observe a high degree of correlation between the two; regression analysis shows that the price correlation coefficient of the two reaches 0.98. Therefore, we can inversely verify our forecast for nickel prices by inferring the future price of nickel sulfate.

Benefiting from the driving effect of ternary materials, the price of nickel sulfate has slowly risen to the current level of ¥25,500 per ton. Meanwhile, it can be observed that the price gap between nickel sulfate and electrolytic nickel (1 ton of nickel sulfate requires 0.22 tons of electrolytic nickel) has further widened, increasing from ¥3,000–¥4,000 per ton at the start of the year to the current ¥7,000–¥8,000 per ton. Overall, the current nickel price is at a historically low level.

From the supply-demand balance of refined nickel between 2006 and 2017, the global refined nickel market remained in a state of oversupply during the period from 2007 to 2015. This gave rise to a long-term decline in nickel prices, and nickel is still mired in a prolonged period of low prices.

A reversal occurred in the supply-demand balance in 2016 and the first half of 2017. In the first half of 2017 alone, the global refined nickel market saw a supply deficit of 50,000 tons, which provided solid support for nickel prices.

China is highly dependent on imports for nickel products, as domestic output falls far short of market demand. Consequently, domestic nickel prices are largely determined by international nickel price trends.

In the second half of 2017 and 2018, the market demand for ternary batteries may rise, which will in turn drive up the demand for nickel sulfate. The market may have already priced in this trend in advance, and the processing fees for nickel sulfate are expected to remain stable. However, the growing demand coupled with falling output of nickel concentrate may lead to a low-level rebound in the price of nickel concentrate.